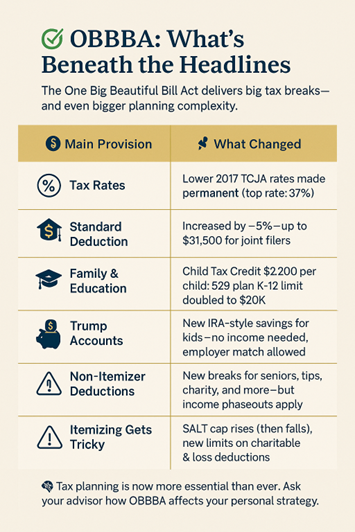

OBBBA: Beneath the Headlines

Taxes Trending TopicsWhile the One Big Beautiful Bill Act (OBBBA) delivers some headline-worthy tax breaks, the underlying rules make tax planning more important — and more complicated — than ever.

Most importantly, key provisions from the 2017 Tax Cuts and Jobs Act (TCJA) were made permanent. Without OBBBA, tax rates, standard deductions, and the estate tax exemption would have reverted to harsher pre-TCJA levels.

OBBBA also introduces dozens of new deductions, credits, and rule changes — but nearly all come with tricky income thresholds, phaseouts, and nuances that make DIY tax prep risky.

Today, we address provisions that impact individuals.

Lower Individual Tax Rates Made Permanent

Without OBBBA, individual tax rates would have reverted to higher pre-2017 levels with a top federal tax rate of 39.6%. With OBBBA, the top rate is 37%.

Standard Deduction Increases by 5%

- $15,750 for single filers

- $23,625 for heads of household

- $31,500 for joint filers

Family & Education Highlights

- Child Tax Credit increased to $2,200 per child (indexed for inflation)

- 529 Plans now cover more K–12 and job training expenses

- K–12 limit raised to $20,000/year (up from $10,000)

- New $1,700 credit (starting 2027) for donations to K–12 scholarship funds (no income limits or phaseouts)

Trump Accounts: A New Kind of IRA for Kids

- Up to $5,000/year per child under 18

- No earned income required

- Investments limited to low-cost index funds (<0.1% fee)

- Employers can contribute $2,500, not taxable to the child

- Children born in 2025–2027 may receive a $1,000 starter deposit from Uncle Sam

- No withdrawals before age 18; distributions follow IRA rules

New Deductions You Can Take Without Itemizing

| ||

Available 2025–2028, with income limits:

| ||

Deduction | Max Amount | Phaseouts / Notes |

|

|

|

Senior Deduction (Age 65+)

| $6,000 individual / $12,000 joint | Starts at $75k / $150k |

Charitable Deduction for Non-Itemizers

| $1,000 single / $2,000 joint | Limited to cash donations; no inflation indexing

|

Tips Deduction | Up to $25,000 | Phaseout begins at $150k / $300k; excludes artists, musicians, entertainers |

|

|

|

Overtime Pay Deduction | $12,500 single / $25,000 joint | Applies only to income above base rate; income phaseouts apply |

|

|

|

Auto Loan Interest | Up to $10,000 | New U.S.-assembled vehicles only; phaseout starts at $100k / $200k |

Itemized Deductions: Still Possible — But Tricky

- SALT (State and Local Tax) Deduction Cap increases to $40,000 in 2025, but phases out starting at $500,000 and reverts to $10,000 in 2030

Heads-up: This phaseout effectively creates a stealth tax increase on households earning $500k–$600k

- Private Mortgage Insurance (PMI) is deductible again (for mortgages up to $750k)

- Charitable Contributions: Beginning in 2026, the first 0.5% of AGI (Adjusted Gross Income) is not deductible

Pro tip: Consider front-loading DAF contributions before 12/31/2025

- Educator Expense Deductions are enhanced — but apply only if you itemize (~10% of all filers)

- Casualty & Gambling Losses: First 10% of losses now ineligible to offset gains

- High-Income Earners: A new “2/37 limitation” reduces itemized deductions for taxpayers above the 37% income threshold

What’s Ending Soon

❌ Clean energy credits for EVs, residential improvements, and solar — all expire after 2025

Final Thoughts

The real impact of OBBBA isn’t in the headlines — it’s in the layers of complexity it adds to the tax code. Many of the new breaks appear generous, but accessing them requires:

- Smart income planning

- Strategic timing

- Coordinated tax, estate, and investment advice

We're here to help you sort through it all. Once updated tax software becomes available, we’ll be ready to run custom tax projections so you can see how OBBBA will affect your personal plan — and what smart moves you can make next.